Stripe's $159 Bi Valuation and Its New Stablecoin Stack

The four-layer money stack that changes everything. How a $1.2B bet and a secret blockchain are rewriting the future of digital payments.

Stripe is in the news (again). With another bump in their valuation, the company is now privately valued at $159 billion. The news comes when their new strategy is starting to consolidate. Their new stablecoin infrastructure isn’t just another crypto play—it’s a complete reimagining of how money moves in the digital economy.

The proof? In the last 24 months, they spent over $1.2 billion acquiring the pieces: Bridge for $1.1 billion and Privy for hundreds of millions. But here’s what most people missed: they’re also building their own blockchain called Tempo. This isn’t experimentation—it’s execution of a master plan.

When the company that processes nearly a trillion dollars annually makes this kind of bet, they’re not following trends. They’re creating them.

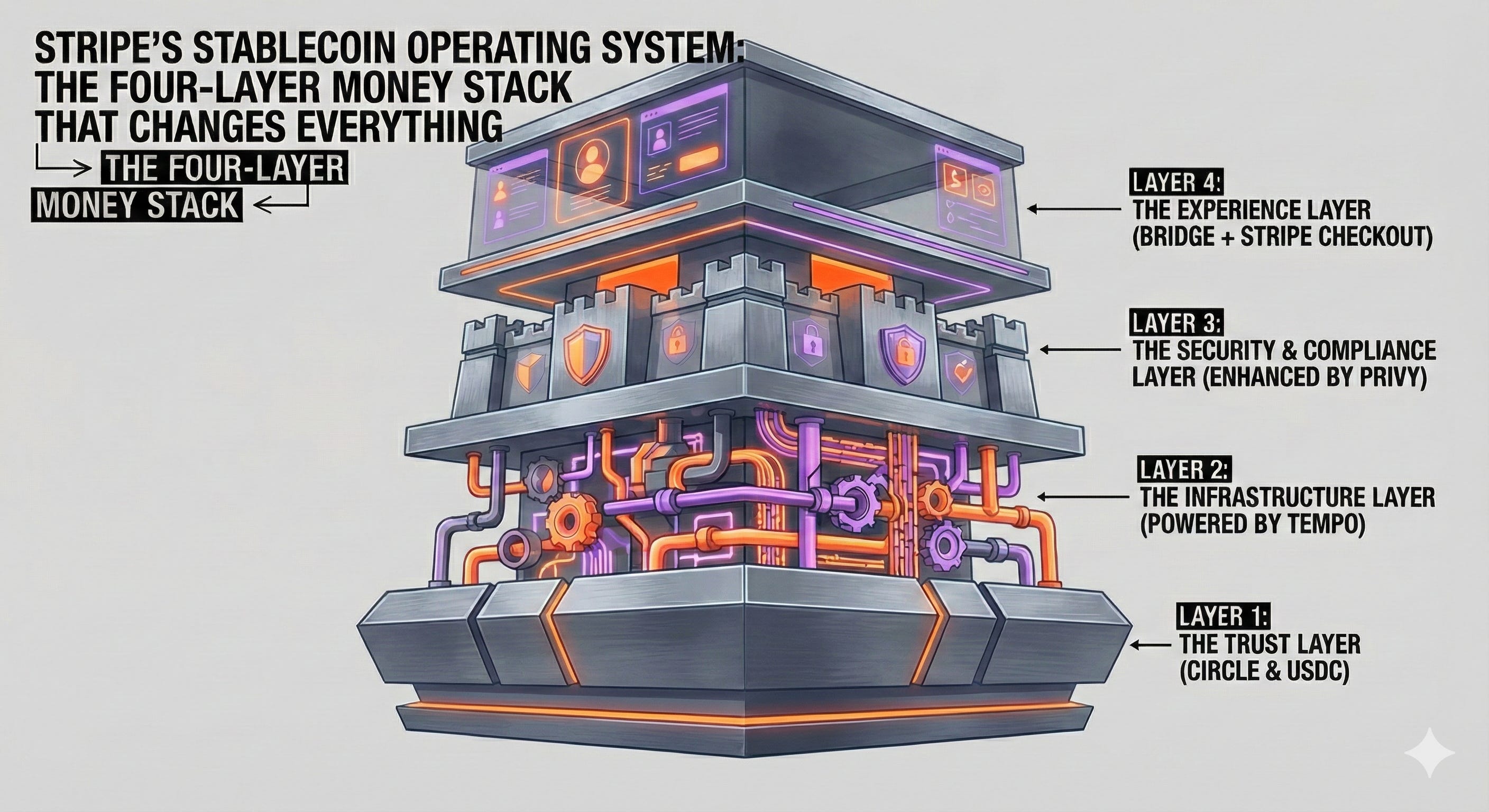

The Four-Layer Money Stack

Stripe’s approach breaks down into four distinct layers, each solving a critical piece of the stablecoin puzzle:

Layer 1: The Trust Layer

This is where most stablecoin projects fail. Stripe partnered with established stablecoin issuers like Circle (USDC) rather than creating their own token. Smart move. They’re essentially saying: “We’re not here to reinvent money—we’re here to make it work better.”

The trust layer handles the messy questions: Is this stablecoin actually backed by dollars? Who’s auditing the reserves? What happens if the issuer goes under? Stripe’s answer: Let the specialists handle stability, we’ll handle utility.

By partnering instead of competing, Stripe avoided the regulatory minefield of stablecoin issuance while gaining access to the most liquid and trusted digital dollars in the market. Circle’s USDC alone has over $35 billion in circulation and regulatory clarity in major markets.

Layer 2: The Infrastructure Layer (Powered by Tempo)

Here’s where Stripe’s secret weapon comes into play: Tempo, their proprietary blockchain infrastructure. While everyone was focused on the Bridge acquisition, Stripe quietly built their own high-performance blockchain optimized specifically for stablecoin transactions.

Tempo isn’t trying to be Ethereum or Solana. It’s purpose-built for one thing: moving money fast, cheap, and reliably. Think of it as AWS for stablecoins—highly available, globally distributed, and optimized for financial workloads.

The key insight? Existing blockchains weren’t built for the payment volumes Stripe processes. When you handle $800 billion annually, you need infrastructure that can scale without compromising on speed or reliability. Tempo gives them that control.

Ethereum processes about 1.2 million transactions daily. Stripe processes over 2 million. The math doesn’t work on public blockchains—especially when your customers expect 99.99% uptime and sub-second response times.

Layer 3: The Security & Compliance Layer (Enhanced by Privy)

The Privy acquisition solves the authentication puzzle. Stablecoins require private key management, but businesses can’t handle the security implications. Privy’s embedded wallet technology lets users interact with stablecoins using familiar login methods—no seed phrases or hardware wallets required.

This removes the biggest barrier to stablecoin adoption: user experience. Instead of managing private keys, users authenticate through methods they already know—email, phone, biometrics. Privy handles the cryptographic complexity behind the scenes.

This layer also handles Stripe’s regulatory moat. They’ve spent 14 years building relationships with financial regulators worldwide. That infrastructure now extends to stablecoins, handling KYC, AML, and cross-border compliance automatically.

Regulatory compliance isn’t just about following rules—it’s about building trust. When Stripe processes a stablecoin payment, it carries the same regulatory rigor as a traditional card transaction. That matters to enterprise customers who can’t afford compliance gaps.

Layer 4: The Experience Layer (Bridge + Stripe Checkout)

This is where the Bridge acquisition becomes critical. Bridge built the best stablecoin API infrastructure in the business—handling multi-chain compatibility, wallet management, and blockchain abstraction. But now it’s supercharged by integration with Stripe’s existing checkout infrastructure.

Imagine checking out on any e-commerce site. Today, you see “Pay with card” or “Pay with PayPal.” Soon, you’ll see “Pay with USDC” right alongside those options. Same familiar checkout flow, but settlement happens in minutes instead of days.

Bridge’s infrastructure handles the technical complexity—automatic gas fee optimization, transaction batching, seamless conversion between different stablecoin standards—while Stripe Checkout handles the user experience. The result? Stablecoins that feel as simple as credit cards.

The integration goes deeper than just adding another payment method. Stripe can automatically convert between traditional currencies and stablecoins at checkout, handle tax calculations across jurisdictions, and provide the same dispute resolution merchants expect from card payments.

Why Tempo Changes the Game

Building their own blockchain might seem like overkill, but it’s actually genius. Here’s why:

Performance Control: Stripe can guarantee transaction speeds and costs because they control the entire stack. No more waiting for Ethereum gas fees to spike or network congestion to clear. They’ve essentially built a private highway for money movement.

Regulatory Clarity: Operating their own blockchain gives Stripe more control over compliance. They can build regulatory requirements directly into the protocol rather than working around existing blockchain limitations. When regulators ask how transactions are processed, Stripe can show them the code.

Integration Depth: Tempo can be optimized specifically for Stripe’s existing products. Automatic reconciliation with traditional banking rails, seamless conversion between stablecoins and fiat, native integration with Stripe’s fraud detection systems. This isn’t possible when you’re building on someone else’s blockchain.

Economic Model: On public blockchains, transaction fees go to miners or validators. On Tempo, Stripe captures that value directly. At their transaction volumes, we’re talking about hundreds of millions in potential revenue.

The Numbers That Matter

Stripe processes over $800 billion annually. If even 5% of that volume shifts to stablecoins, we’re talking about $40 billion in new stablecoin transaction volume. That’s roughly doubling the current market.

But here’s the real kicker: Stripe’s international payment volume is growing 50% year-over-year. Traditional cross-border payments are expensive and slow—exactly what stablecoins solve. The addressable market isn’t just existing volume, it’s unlocking entirely new use cases.

Consider the math on cross-border payments:

- Traditional wire transfers: 2-5 days, 3-7% fees

- SWIFT payments: 1-4 days, 1-4% fees plus FX spreads

- Stablecoin payments via Stripe: Minutes, sub-1% fees

For a $100,000 international payment, businesses could save $2,000-6,000 in fees and get their money days faster. Multiply that across millions of transactions, and you understand why Stripe bet $1.2 billion on this infrastructure.

The Stripe Advantage

Other companies are building stablecoin infrastructure too. So why does Stripe win?

Distribution: They already have relationships with millions of businesses worldwide. Those businesses trust Stripe with their money. That trust transfers to stablecoins. When Stripe adds stablecoin support to their dashboard, millions of merchants get instant access.

Full Stack Control: From blockchain (Tempo) to security (Privy) to APIs (Bridge) to user experience (Checkout), Stripe owns every layer. That integration creates competitive moats competitors can’t easily replicate. It also means faster innovation—they don’t need to coordinate with external partners to ship new features.

Regulatory Relationships: Getting money transmitter licenses in all 50 states isn’t just expensive—it’s a multi-year process requiring millions in compliance costs. Stripe already paid that price and built those relationships. New entrants have to start from zero.

Network Effects: The more businesses use Stripe’s stablecoin infrastructure, the more valuable it becomes. Businesses that receive USDC payments through Stripe can more easily make USDC payments to their suppliers. This creates a self-reinforcing cycle that’s hard for competitors to break.

What This Means for Business

If you’re running a business that moves money internationally, pay attention. Stablecoins through Stripe could cut your settlement times from days to minutes and your fees from 3-5% to under 1%.

But more importantly, this infrastructure makes new business models possible:

Instant Global Payroll: Pay remote workers anywhere in the world, instantly, without traditional banking delays. No more explaining to contractors why their payment is “processing” for a week.

Real-time Revenue Sharing: Automatically distribute revenue to partners the moment transactions clear. Imagine affiliate commissions paid instantly instead of monthly.

Programmable Payments: Smart contracts that execute automatically based on business logic. Pay suppliers when goods are delivered, release funds when milestones are met, split payments between multiple parties automatically.

Micro-transaction Economics: Traditional payment rails make small transactions uneconomical. Stablecoins enable new business models around micro-payments, subscription tiers under $1, and pay-per-use services.

The Competitive Landscape

Stripe isn’t alone in this space. PayPal has PYUSD, Visa is building stablecoin settlement rails, and dozens of crypto-native companies are fighting for market share. But Stripe’s approach is different in three key ways:

Enterprise Focus: While others chase consumer adoption, Stripe built enterprise-grade infrastructure first. Their customers need reliability, compliance, and integration depth—not flashy features.

Infrastructure Investment: The $1.2 billion in acquisitions plus Tempo development represents the largest single bet on stablecoin infrastructure by a traditional fintech company. That level of investment creates capabilities competitors can’t match quickly.

Proven Execution: Stripe has a track record of taking complex financial infrastructure and making it simple for developers to use. They did it with online payments, payouts, and subscription billing. Stablecoins are the natural next step.

The Regulatory Wild Card

The biggest risk to Stripe’s stablecoin strategy isn’t technical—it’s regulatory. Stablecoins exist in a gray area in many jurisdictions, and rules are evolving rapidly.

But this is where Stripe’s 14-year head start matters. They’ve navigated regulatory challenges in dozens of countries, built relationships with central banks and finance ministries, and proven they can operate complex financial infrastructure compliantly.

More importantly, Stripe’s approach reduces regulatory risk by partnering with licensed stablecoin issuers rather than issuing tokens themselves. They’re the infrastructure layer, not the money issuer. That distinction matters to regulators who are still figuring out how to classify different crypto activities.

The Global Implications

If Stripe succeeds, they won’t just change how businesses move money—they could reshape global financial infrastructure. Stablecoins that settle instantly and cost almost nothing to transfer could reduce friction in international trade, enable new forms of economic cooperation, and extend financial services to underserved markets.

Consider the implications for developing economies where traditional banking is expensive and unreliable. A small business in Kenya could receive payment from a customer in Germany and immediately pay suppliers in China—all settled in minutes for minimal fees. That’s not possible with traditional correspondent banking.

This infrastructure could also enable new forms of programmable money. Smart contracts that automatically escrow funds, release payments based on real-world events, or split revenue between multiple parties. These capabilities exist in crypto today but require technical expertise most businesses don’t have. Stripe’s infrastructure makes them accessible to any developer.

What Comes Next

Stripe’s stablecoin infrastructure is still in early stages, but the pieces are falling into place rapidly. Bridge is already processing millions in monthly volume, Privy’s wallet technology is being integrated across Stripe’s product suite, and Tempo is handling initial transaction loads.

The real test will come when Stripe starts migrating significant portions of their existing payment volume to stablecoin rails. That migration won’t happen overnight—it requires merchant adoption, regulatory clarity, and user education. But when it does happen, it will represent one of the largest shifts in payment infrastructure in decades.

For businesses, the smart move is to start experimenting now. Understanding how stablecoin payments work, what the tax implications are, and how they integrate with existing financial processes will provide competitive advantages as this infrastructure scales.

For developers, Stripe’s API-first approach means stablecoin functionality will be as easy to integrate as traditional card payments. The same few lines of code that power e-commerce today will soon enable instant, global, programmable money movement.

The Bigger Picture

Stripe isn’t just building better payment rails—they’re building the financial infrastructure for the next decade of global commerce. That $1.2 billion investment, plus the development of Tempo, signals they’re all-in on making it happen.

The implications extend far beyond Stripe’s business. If they succeed in making stablecoins as easy to use as credit cards, they’ll accelerate adoption across the entire fintech ecosystem. Other payment processors will be forced to follow suit, traditional banks will need to offer stablecoin services, and businesses worldwide will gain access to programmable, instant, global money movement.

This isn’t just about payments—it’s about unlocking new forms of economic coordination. When money can be programmed, transferred instantly, and settled globally without intermediaries, entirely new business models become possible.

The question isn’t whether stablecoins will become mainstream payment infrastructure. Stripe just answered that with a $1.2 billion exclamation point. The question is how quickly the rest of the industry will catch up—and what new possibilities emerge when money moves at the speed of the internet.

When the dust settles, Stripe’s four-layer money stack might be remembered as the infrastructure that brought digital money to the masses. Not through speculation or hype, but through the same methodical, developer-focused approach that made them the backbone of internet commerce.

That’s how revolutions really happen: not with a bang, but with infrastructure so good that using anything else feels obsolete.